How It Works

The Three-Layer Collateral Solution

Halden's three-layer collateral architecture directly addresses the exposure gap that makes traditional GPU financing untenable. By combining physical GPU collateral, growing cash reserves, and collateral insurance, the structure maintains comprehensive lender protection at every stage of the loan lifecycle, all without forcing borrowers into punishing down payments or unsustainable payment obligations. Finally, cash reserves built during the loan term are returned to the borrower at maturity – something no other financing offers.

Physical Collateral

Cash Collateral

Collateral Insurance

The Core Challenge, Revisited

Traditional GPU financing fails because a single layer of physical collateral (the GPU hardware itself) cannot maintain adequate value relative to the outstanding loan balance as technology advances. The exposure gap that opens up is real credit risk. Traditional lenders respond with terms that eliminate exposure by effectively eliminating the deal.

Halden's approach doesn't pretend the risk doesn't exist. It systematically eliminates the exposure through three complementary layers of collateral protection that evolve together throughout the loan lifecycle.

Layer 1: Physical Collateral — The Foundation

Every GPU financing structure begins with the GPU servers themselves. At loan origination, these assets represent the primary collateral - real, tangible hardware with established market prices, active resale markets, and predictable utility in AI workloads.

Physical collateral is strongest early in the loan term, when the hardware is newest and closest to its purchase price. As technology advances, this layer alone faces the depreciation challenge. In Halden's framework, it is the foundation - the starting point upon which two additional layers of protection are built.

Layer 2: Cash Collateral — The Game-Changing Innovation

The second layer is where Halden's approach becomes genuinely distinctive: a portion of each monthly payment builds a cash reserve account that serves as growing collateral. Think of it as a structured investment program embedded within the loan itself.

As the loan progresses, cash reserves accumulate month by month, creating a powerful dynamic. While the physical hardware is losing value due to technological advancement, the cash collateral pool is growing, progressively shifting risk away from depreciating GPUs toward appreciating cash.

Extending the loan term makes this work. Longer duration creates the room to build meaningful cash reserves without creating unsustainable monthly payment burdens. This is why longer terms aren't just borrower-friendly, they're structurally necessary for the cash collateral strategy to function.

Critically, these cash reserves belong to the borrower. They are held in a secure investment account as collateral for the lender during the loan term, then returned at maturity. This provides the borrower with substantial capital for the next growth phase, equipment upgrades, or other business needs. The cash collateral is not simply a cost of financing; it builds a meaningful asset that comes back to the borrower at term end.

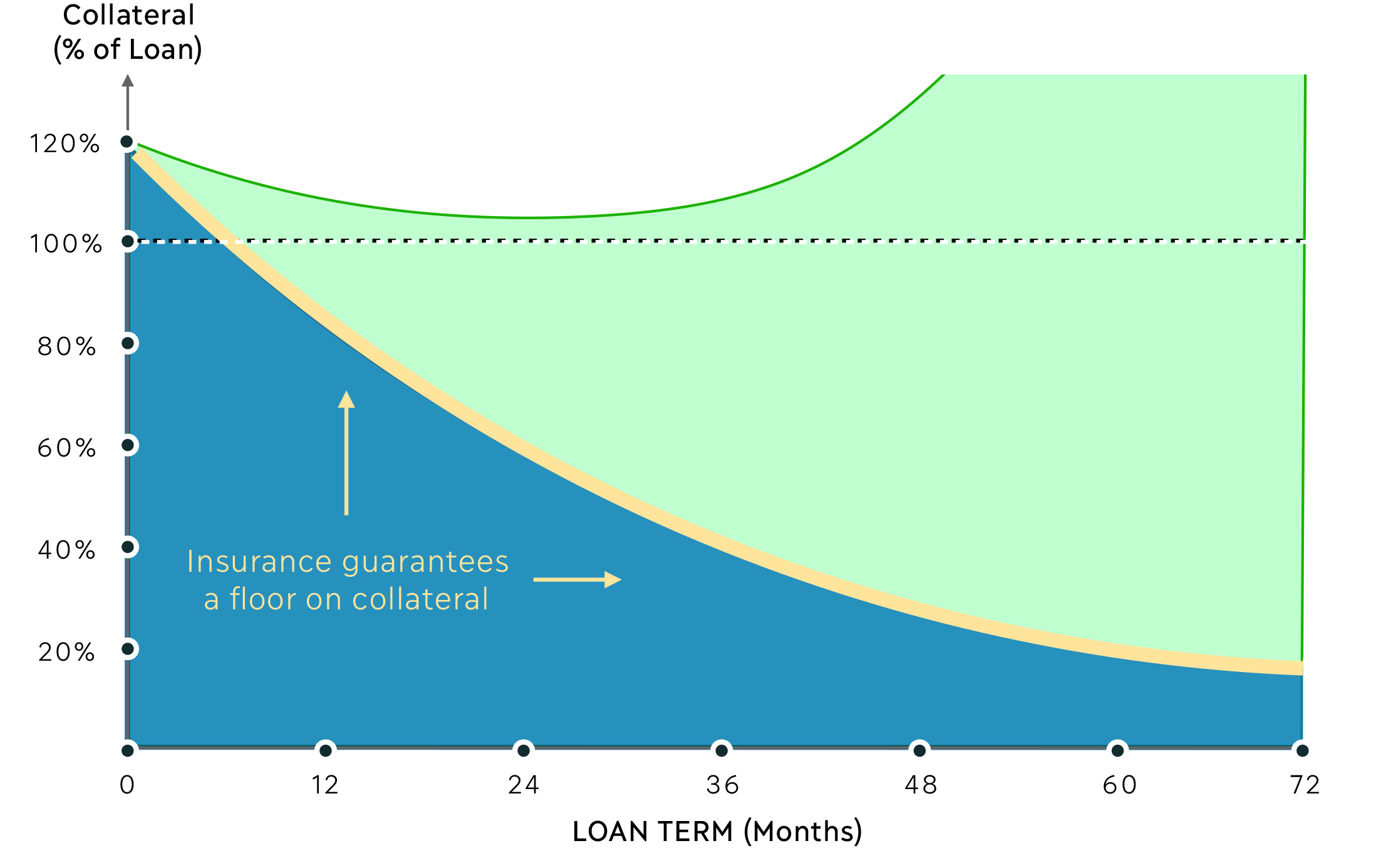

Layer 3: Collateral Insurance — The Guaranteed Floor

The third layer addresses the ultimate lender concern: what if depreciation is worse than projected? What if a breakthrough in GPU architecture causes values to collapse faster than anticipated, or secondary markets seize up during a market dislocation?

Collateral insurance establishes a guaranteed floor on GPU liquidation value. If a default occurs and GPUs need to be liquidated, the insurance ensures the lender will recover at least a minimum value, regardless of prevailing market conditions. Think of it as the equivalent of guaranteed residual values in auto leasing, specifically engineered for GPU hardware.

The Three Layers Working Together

The three layers are designed to evolve across the loan term, with the composition of protection shifting as the loan matures:

- Early months: Physical GPU collateral provides the majority of protection. The hardware is nearly new, worth close to its purchase price. Cash reserves are beginning to accumulate.

- Middle of the loan: Two things happen simultaneously. GPU values gradually decline while cash collateral steadily builds. The transition progressively shifts protection from depreciating hardware to growing cash reserves.

- Final phase: Cash collateral provides the majority of protection. Accumulated reserves can cover the remaining loan balance independently. The insurance layer provides final backstop protection for extreme scenarios.

The result: at every point in the loan term, the combined three-layer collateral structure protects the outstanding loan balance. There is almost no exposure gap. The risk that made traditional GPU financing structurally unworkable has been systematically engineered away.

What This Means for Capital and AI Clouds/Startups

For lenders (capital providers), the structure provides comprehensive risk mitigation across multiple failure scenarios, progressive de-risking as cash collateral builds, downside protection through insurance guarantees, and multiple recovery mechanisms if a default occurs.

For borrowers (AI clouds and startups), this structure enables higher loan-to-value ratios, longer loan terms with lower monthly payments, cash reserves returned at maturity, and the ability to access financing without requiring signed customer contracts as a precondition. Growth becomes possible without continious and equity dilution.