The root of the Problem

Why Traditional Financing Fails GPU Financing

The AI industry faces a fundamental capital constraint - not a shortage of technology or demand, but a shortage of financing designed for GPU infrastructure. Traditional lenders apply frameworks built for cars and construction equipment to hardware with unique dynamics, producing terms that protect lenders but become the primary bottleneck to growth.

Halden was built to solve this.

Capital is the Bottleneck Holding Back AI Compute

The AI age has arrived, but the capital required to support it has not. AI companies need large fleets of GPUs to meet surging customer demand, yet traditional financial institutions still treat GPUs like experimental assets rather than critical infrastructure.

The result is a classic chicken-and-egg problem: lenders require signed customer contracts before financing GPUs, while customers won't commit until compute is installed and operational. To break the deadlock, many AI cloud providers are forced into highly dilutive equity rounds. Smaller providers are often left to fund their fleets entirely from cash - an approach that doesn't scale and frequently stalls expansion.

Access to capital - not technology or customer demand - is the primary constraint on AI compute expansion.

The Obsolescence Challenge

At the root of the GPU financing gap lies a mismatch between how traditional lenders assess risk and how GPU hardware actually behaves. Unlike tractors, aircraft, or construction equipment (assets that maintain substantial residual value for decades), GPU technology advances in generational cycles measured in years.

Each new chip architecture can deliver meaningful performance improvements that reduce the competitive standing of previous generations. This creates a concern that traditional lenders can't easily model or diversify away: correlated depreciation risk. When a new, more powerful chip generation launches, it can affect the resale value of every GPU in a lender's portfolio simultaneously.

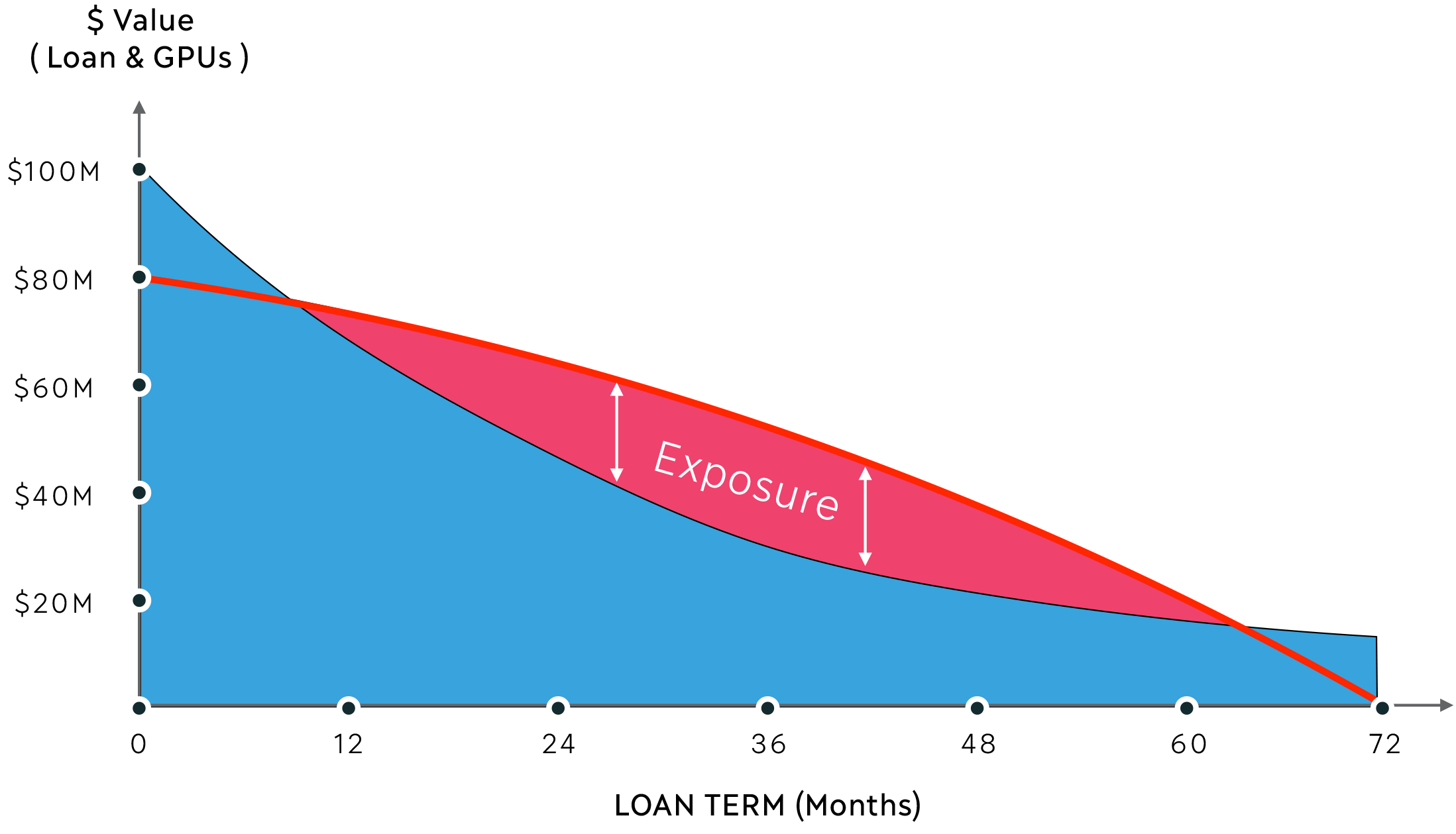

The Exposure Problem

In conventional equipment financing, collateral value ideally declines at roughly the same pace as the outstanding loan balance. With GPUs, that alignment breaks down.

When you plot a GPU's declining market value against an amortizing loan balance, a gap opens up, which we call the "exposure zone." For much of the loan term, the outstanding balance exceeds what a lender could recover by liquidating the equipment. This isn't a theoretical risk. It represents genuine economic exposure that traditional lenders cannot easily absorb across a portfolio.

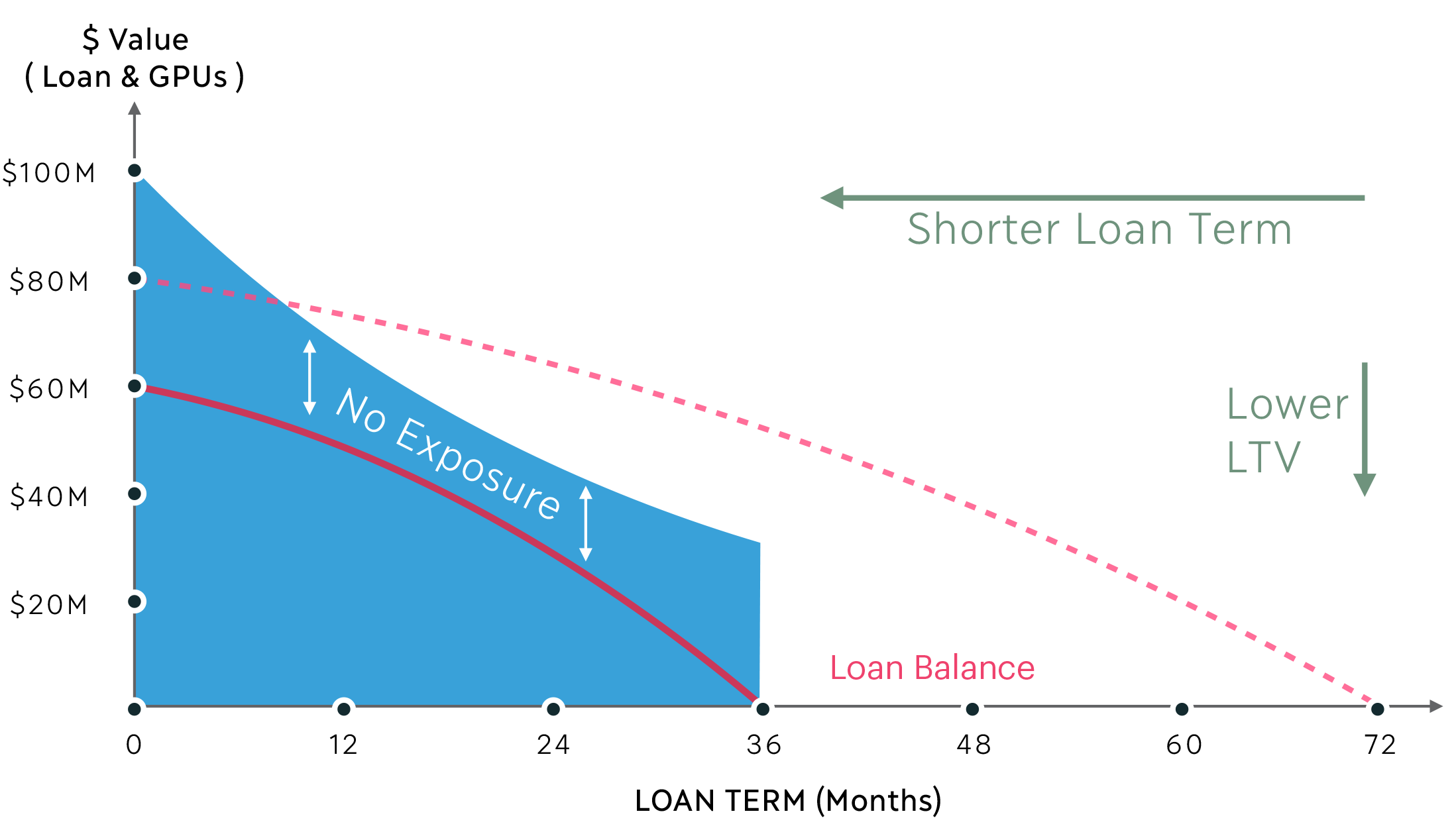

The Conservative Response and Why It Fails

Faced with this exposure challenge, traditional lenders respond by dramatically tightening lending terms: slashing loan-to-value ratios, shortening loan durations, and requiring signed customer contracts before approving any financing.

These measures protect the lender but create a challenging situation for borrowers. Lower LTV ratios mean steep upfront capital requirements. Shorter loan terms mean elevated monthly payments that strain cash flow.

This is the fundamental Catch-22: terms strict enough to be safe for lenders are terms difficult to accept for borrowers.

Recognizing the Real Infrastructure Challenge

Solving this requires rethinking the entire financing structure from the ground up. The obsolescence problem is real. The exposure gap is genuine. Traditional financing structures genuinely don't work for assets with this depreciation profile.

What's needed is a purpose-built framework that takes these challenges seriously. That means building in multiple layers of protection, shifting collateral composition as the loan matures, and structuring payment flows that work for both lenders and borrowers.

This is the problem Halden was built to solve.